Generative AI is very useful. It can summarize conversations, draft emails, write code, and even generate images and video. I believe it will eventually have a profound impact on the world. At the same time, I also believe most AI stocks are in an over-hyped bubble. For a revolutionary technology to be a stock market bubble is not contradictory, but rather the norm. If we look at stock market history, most revolutionary technologies were accompanied by stock market bubbles. This was true with the advent of automobile and the radio in the early 20th century and the early days of the internet in the late 1990s. The fault is not with the technology, but with us as people. Humans tend to become overly optimistic on the pace of adoption for new technologies, which ultimately set up unrealistic expectations ripe for disappointment. Wearing rose colored glasses, we overlook flaws such as the lack of profitability.

In the stock market, this manifests as a speculative orgy as investors fearful of missing out crowd into anything that is AI-related. While Nvidia is the poster child of AI, the AI-bubble has lifted all semiconductor stocks from AMD to Broadcom. Even Dell managed to get in on the action. People forget that semiconductor companies are deeply cyclical and what is this year’s robust orders could quickly disappear next year. In the late 1990s, adding “.com” was sufficient to lift a stock. Today, you just need some credible link to AI.

Setting aside all the fake AI stocks, even real beneficiaries of AI such as Nvidia suffer from bubble valuations. This is because the pace of how quickly these stocks have risen far exceeds the realities of adoption and profitability.

Below I include the stock charts of Nvidia and Super Micro, two semiconductor companies seeing robust sales growth from AI-driven demand.

Both stocks have gone up a lot. Note the acceleration and much steeper slope post Jan 2024. These stocks recently exhibited a hockey-stick-like upward inflection. SMCI’s stock has gone up 3.5x in just the past three months. This kind of melt-up chart is one of the telltale signs of a FOMO driven mania.

This becomes even more evident when we compare these stock charts with reality on the ground. The following shows U.S. Google search volume for “ChatGPT”. ChatGPT did truly explode out of the gate. It went from zero to impressive search volumes in just a few months. However, since peaking in April of 2023, search volume has been largely sideways. This suggests that while initial adoption was strong, the growth of new users has since slowed.

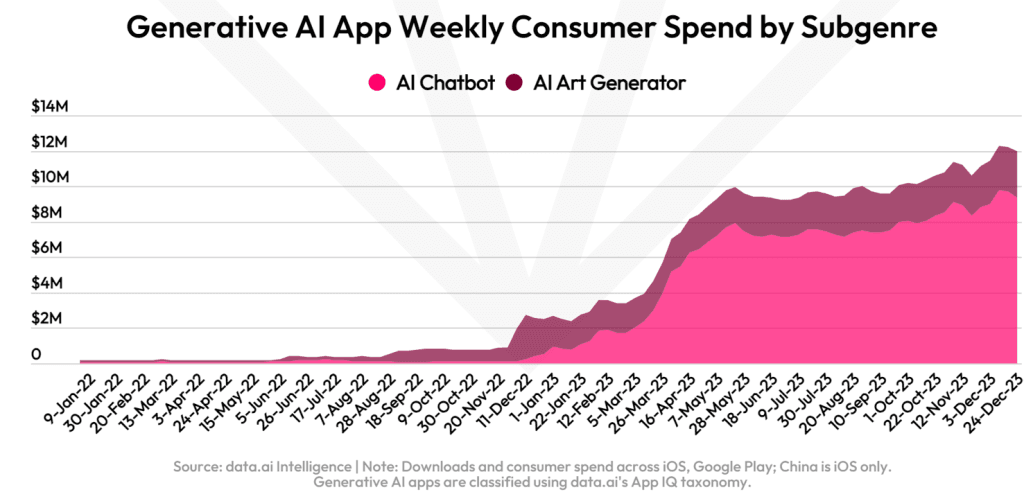

The following chart of consumer spending across all generative AI apps on mobile phones shows a similar pattern. We saw explosive growth out of the gate, but much more measured growth since April of 2023.

The next chart shows ChatGPT’s iPhone app store grossing ranking in the US. There is a steady upwards trend, but certainly no hockey stick growth. And a grossing ranking of 50-70 is relatively low in the grand scheme of things and puts ChatGPT’s mobile grossing on par with apps such as Big Fish Casino and Solitaire Grand Harvest.

Whether it is Google search traffic or mobile app data, the message is clear. After exploding out of the gate, generative AI’s new user acquisition growth has slowed significantly. The good news is that there is some modest growth and decent retention for existing users. The bad news is that after quickly attracting tech-savvy early adopters, generative AI is finding it much harder to win new users.

If the consumer adoption of generative AI has slowed, perhaps the enterprise use cases are getting more traction? After all, Microsoft did spend millions of dollars to feature Microsoft Copilot in a Superbowl ad. Wall Street Journal reported on the experience of companies who have been testing Copilot. The article was lukewarm at best, calling Copilot “useful, but doesn’t live up to its price” at $30 a head per month. This was the conclusion of Juniper Networks chief information officer Sharon Mandell who said “I wouldn’t say we’re ready to spend $30 per user for every user in the company.” Others have been more critical with Andreessen Horowitz partner Guido Appenzeller calling PowerPoint’s CoPilot integration “a mess and not anywhere close to adding value.” Lenovo also noted that aside from the AI used to transcribe meetings on Teams, there was about a 20% drop in the use of Copilot for most software after a month.

CoPilot’s U.S. iPhone app store grossing rankings are not particularly encouraging either with grossing rankings steadily declining since the Superbowl ad.

What about using AI to increase productivity for uses cases such as game design? In theory, generative AI should be able to assist in game development and the creation of NPCs (non-playable characters). Asked about the potential benefits of AI, gaming giant Tencent said AI would one day benefit game developers, but we are years not months away from seeing any meaningful benefits.

How about using AI to generate advertising creatives? Lego recently apparently tried this with images of Ninjago characters on its website. Unhappy Lego fans accused the toy maker of using AI to generate character that are oversaturated, impossibly shiny, and occasionally with extra fingers. The AI-generated images were swiftly removed from the website and Lego issued a statement saying, “These images were used in a test, which happened outside of our usual approval process, and we will take all necessary steps to ensure that it won’t happen again.” Wall Street Journal reports that creatives have to rely on scores of professionals to edit the images AI generates to avoid that “AI look.” AI-generated images will no doubt improve in the future, but, as of today, hype is still greater than reality.

If end user demand is somewhat tepid, why is Nvidia revenues skyrocketing? I believe it is because companies both large and small are racing to build and train competing generative AI models and applications in anticipation of skyrocketing demand. Whenever there is a shortage of chips, companies also tend to double and triple their orders to try to get larger allocations. If end demand grows slower than people expect, we might go quickly from a shortage into a surplus.

Another reason generative AI is at the hype phase is that there is still not a clearly defined business model. As far as I can tell, all the AI companies lose money. In a presentation earlier this month, the venture-capital firm Sequoia estimated that the AI industry spent $50 billion on the Nvidia chips used to train advanced AI models last year, but brought in only $3 billion in revenue. Until AI figures out an attractive and profitable business model, it appears to be mainly dumping capital into a black hole.

Even if AI demand remains strong, Nvidia still has a major issue: competition. Today, Nvidia is a virtual monopoly on the graphics chips needed for generative AI. Further, due to the shortage of chips, Nvidia is charging an arm and leg for its chips and making an incredible 80% gross margin (up from mid 50s% just a year ago). Jeff Bezos famously said, “Your margin is my opportunity.” Nvidia simply cannot sustain these margins in a competitive capitalist system. Competitors such as AMD are salivating at those margins and racing to catch up. Nvidia’s hyperscaler customers such as Microsoft, Amazon, Google and Meta are all incentivized to either develop their own chips in-house or support a viable competitor. Recently, Reuters reported that a group formed by Intel, Google, Arm, Qualcomm, and Samsung is working on developing an open-source software suite that prevents AI developers from being locked into Nvidia’s proprietary technology.

Nvidia is in many ways priced for perfection today. Investors dream of unsatiable AI demand while enjoying mouthwatering 80% gross margins. The real world is rarely that perfect. Storm clouds are usually just around the corner.

Nvidia today reminds me of Tesla in late 2021. At that time, the enthusiasm over the exploding demand for electric vehicles (another revolutionary technology) sent Tesla on a similar hockey-stick run-up to $400 per share. With little competition, Tesla was making industry leading 30% gross margins. Investors who had FOMO and chased Tesla and the hot EV trend were in for a rude awakening. In the two years since, competition has increased significantly and EV demand grew slower than anticipated. Forced to cut prices to move units, Tesla’s gross margins collapsed to 16%. Despite these price cuts, Tesla’s unit growth is stalling and units actually declined year over year in the first quarter of 2024. As for the stock price, it is down 60% over the past two and a half years. There just might be a lesson in there for Nvidia investors.

Disclosure

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I do not have an investment in NVDA shares.

The information in the article is provided for informational purposes only. It should not be construed as investment advice or advice on buying, selling, or other types of transactions relating to an investment in products or services, much less an invitation, an offer or a solicitation to invest.

The information in the article is provided solely by virtue of the fact that everyone will independently make their own investment decisions: the report does not take into account investment objectives, nor specific needs or financial situation. In addition, nothing in the article represents or is intended to express investment, financial, legal, accounting or tax advice. You should consult your own investment or financial advisor before taking any actions.